Interest payments have risen by the most on record.

There is a way out of almost every economic difficulty:

Higher productivity.

A country beset with immense debt can indeed grow its way out of the problem, but only if productivity is rising at a substantial pace.

Unfortunately, that kind of growth would require a low-tax, pro-business economic environment.

And that’s not what we have in Canada.

Thus, we are seeing financial problems mounting, with more and more concerning date emerging.

Household debt rises

The household debt-to-income ratio reached 1.83, up slightly from the second quarter of 2022, and an increase from 1.77 a year ago.

This brings the ratio to just below the record of 1.84.6%.

The combination of recent interest rate hikes, combined with the high rate of household debt, has led to a record increase in interest payments.

Interest payments rose 16.2%.

Unsurprisingly, this also led to an increase in the debt-service-ratio, which is now 13.97%, up from 13.46% in Q2.

At the same time, net worth per capita fell 3.8%.

Bank regulator raises stability buffer

The rise in interest costs and high consumer debt clearly concerns Canada’s top financial regulator.

Last week, the Office of the Superintendent of Financial Institutions is increasing the bank stability buffer.

As indicated by reports, the OSFI says “the domestic stability buffer will go up by half a percentage point to three per cent as of Feb. 1, 2023. It also increased the possible range of future adjustments to between zero and four per cent, rather than the previous top end of 2.5 per cent.

The adjustment comes as debt levels and delinquencies remain fairly stable while debt service costs are on the rise, OFSI chief risk officer Angie Radiskovic told reporters.

“Clearly, we’re in a risk environment now where levels of indebtedness have grown. We’ve got high inflation, we’ve got rising interest rates and a lot of our thinking is holding around those types of risks,” Radiskovic said.

By raising the amount of money banks need to set aside, it gives the regulator more room to lower the capital requirements when a downturn hits to give banks access to potentially needed extra funds.”

Stagflation nation

As noted at the outset of this column, Canada could escape these challenges if we had a high level of productivity.

Just a like a company that borrows heavily can sustain that borrowing if it is rapidly becoming more efficient and is expanding in scale, a country can sustain a growing debt burden if per capita GDP is going up substantially.

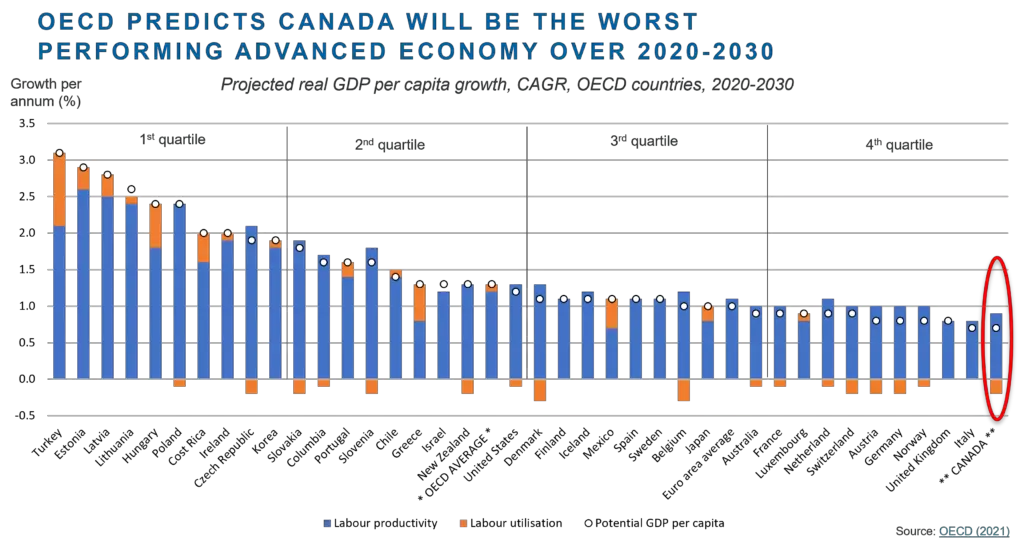

But here in Canada, our productivity – as measured by per capita GDP – is projected to be the lowest in the OECD:

Policies like the carbon tax, and the rejection of opportunities we could have had – like selling vast quantities of LNG to Germany – end up trapping Canadians in our highly-indebted circumstances.

If we can’t increase productivity, then we will remain mired in stagflationary circumstances, where debt goes up, costs rise, but growth can’t keep up.

Spencer Fernando

***

If you value my independent & rational perspective, you can contribute to support my work through PayPal or Stripe below.

PAYPAL

[simpay id=”28904″]